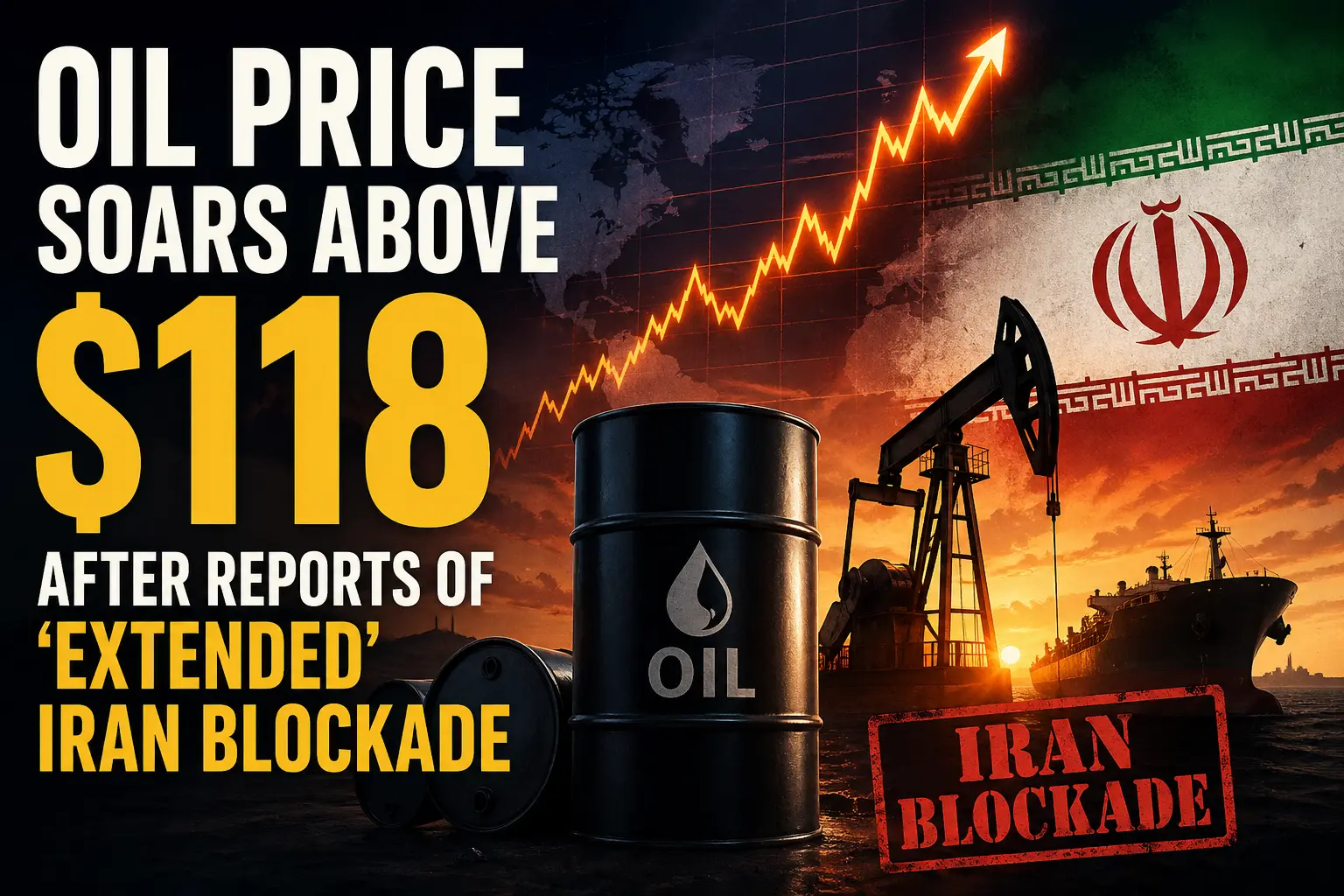

Oil prices surged sharply on Wednesday, with Brent crude climbing above $118 a barrel after reports that the United States could extend its blockade on Iran, intensifying fears of a prolonged supply shock in global energy markets. The move pushed crude to its highest level in nearly a month and reignited concerns over inflation, transport costs, and fuel prices worldwide.

According to market reports, traders reacted after new signals suggested the blockade on Iranian ports may continue longer than previously expected. Iran remains a key oil producer, and any disruption to exports from the Gulf region immediately impacts global supply expectations. Investors are especially concerned because the Strait of Hormuz, one of the world’s most important oil transit routes, remains under pressure amid ongoing tensions.

Brent crude futures rose more than 6% to $118.33, while U.S. West Texas Intermediate (WTI) also jumped above $105. Analysts said the rally was driven not only by geopolitical risk but also by fresh U.S. inventory data showing a larger-than-expected drop in crude stockpiles, indicating tighter supply conditions.

Higher oil prices could quickly translate into rising petrol and diesel costs for consumers, especially in import-dependent countries such as India and many European nations. Airlines, shipping firms, and manufacturing sectors may also face higher operating expenses if prices remain elevated.

Markets are now watching whether diplomatic efforts between Washington and Tehran can resume. Any sign of easing tensions could cool prices, while an extended blockade or military escalation may send crude toward $120 or higher.

The latest surge highlights how vulnerable global energy markets remain to geopolitical disruptions. With inflation already a concern in many economies, sustained high oil prices could create fresh challenges for central banks and policymakers in the weeks ahead.